From Regulatory Approval to Flexible Financing: Standards Mapping in Integrated Wagering Networks

Authorization standards in wagering networks establish the rules that determine which payment methods operators may accept while maintaining compliance across multiple jurisdictions, and this mapping process directly shapes the range of funding options available to users on integrated platforms that combine sports betting with casino offerings. Regulatory bodies require operators to verify identity, source of funds, and transaction limits before approving any deposit channel, which creates a direct relationship between the rigor of those checks and the speed or variety of funding methods that become accessible.

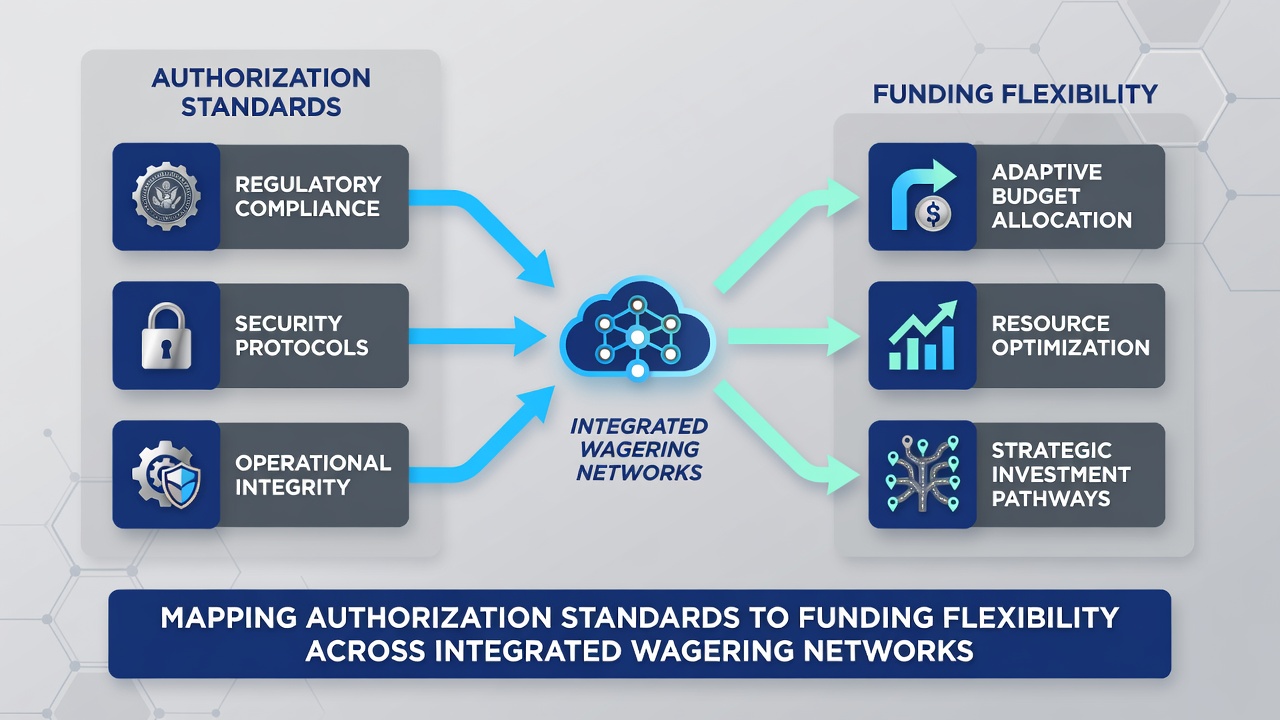

Core Components of Authorization Frameworks

Authorization frameworks typically include licensing requirements, know-your-customer protocols, and ongoing monitoring mandates that vary by region yet share common data points such as age verification, address confirmation, and financial history screening. When these standards align with payment processor capabilities, platforms gain the ability to offer instant bank transfers, e-wallets, and prepaid cards without triggering additional reviews, whereas stricter or mismatched standards force delays or exclusions for certain methods.

Those who have examined cross-border operations note that networks spanning multiple states or countries must reconcile differing authorization thresholds, for example by applying the highest standard across all connected systems to avoid regulatory gaps. This reconciliation process often results in standardized APIs that automatically route transactions through approved channels based on user location and account status.

Funding Flexibility Outcomes

Platforms that successfully map authorization standards to funding tools experience measurable increases in transaction success rates because users encounter fewer rejections at the deposit stage. Data from integrated networks shows that operators who embed compliance checks directly into payment gateways can activate additional methods such as cryptocurrency options or instant ACH transfers once initial verification clears, whereas fragmented systems limit users to slower bank wires until manual reviews complete.

What's interesting is how June 2026 updates to interstate compact agreements have prompted several networks to revise their mapping procedures, allowing approved operators to extend flexible funding across state lines when authorization records remain synchronized through shared databases. This adjustment has enabled certain platforms to introduce region-specific bonuses tied to verified payment histories without separate approval steps for each jurisdiction.

Technical Integration Challenges

Integrated wagering networks rely on centralized ledgers that record authorization status alongside transaction metadata, which allows real-time decisions on whether a funding request meets all applicable standards before processing. Developers build these systems using modular code that separates identity verification modules from payment routing logic, making it easier to update one without disrupting the other when regulations change.

Yet mismatches still occur when legacy payment processors operate outside the main authorization layer, forcing operators to maintain parallel approval paths that reduce overall funding flexibility. Observers note that networks investing in unified APIs have reduced such friction, resulting in quicker activation of new methods once regulators certify the updated compliance mapping.

Regional Examples and Adjustments

In North America, operators working under compacts between states have adjusted their authorization protocols to accommodate varying funding rules, such as those governing prepaid card usage in one jurisdiction versus digital wallet acceptance in another. European platforms, guided by requirements from the European Gaming and Betting Association, have mapped similar standards to support cross-border transfers while respecting local restrictions on certain high-risk payment types.

One documented case involves networks that adopted shared verification tokens, allowing users who clear authorization in a primary market to access expanded funding options in secondary markets without repeating full screening. Such approaches have proven effective in reducing drop-off rates during the deposit process across connected platforms.

Conclusion

Mapping authorization standards to funding flexibility continues to evolve as networks expand and regulators refine their expectations around transaction monitoring and cross-jurisdictional data sharing. Operators who maintain synchronized compliance layers gain broader payment capabilities, while those facing fragmented standards encounter persistent limitations on which methods they can offer at scale. The relationship between approval processes and available funding channels remains central to how integrated wagering systems serve users across different regions and regulatory environments.